First, let’s explain some of what is behind the recent market rally. Perhaps the most important factor in the stock market’s rise this year has to do with recent actions by the European Central Bank (ECB). In December, amidst a brewing economic and banking crisis, the ECB offered European banks the opportunity to borrow unlimited amounts of money for 3 years at an interest rate of 1%. The reason for this Long Term Refinancing Operation (LTRO) was clear. Fears of insolvency, resulting from concentrated investments in potentially bad debt from certain European countries, had closed access to the credit markets for many European banks. Where no money could be found, the ECB turned on the printing press.

What the ECB did is important. In both Europe and the United States, central banks continue to fill the void in credit markets as the world economy recoils from a massive debt bubble. Perhaps in the short-term, by taking financial collapse off the table, we are better off. Even though the US stock market had zero return last year, the Federal Reserve’s launch of QE 2 in August of 2010 provided a powerful rally from that point until May of 2011. That rally was very similar in cause, magnitude, and character to the current rally.

Clearly central banks are buying time for policy makers to adapt and economies to adjust. Yet, it is necessary to remain aware of how much support is provided by their actions. The Federal Reserve has injected more than $2.5 Trillion into U.S. Treasuries and Mortgage Backed Securities since 2008. With LTRO alone, the ECB provided almost $700 Billion to support European banks.

As a result, the equity markets, which were starting to price in financial meltdown in Europe, are now pricing in a more optimistic view. Expectations have quickly turned positive with bullish sentiment of stock market forecasters approaching historically high levels. We have seen a significant rally in “low-quality”, beaten-down stocks, as they recover from last year’s lows. While those stocks have led the market, there has been a broad advance in US equity indexes, supported in part by decent economic data in the US.

With expectations for support from global central banks every time a problem appears, it seems likely that markets could hold up reasonably well this year. However, we would like nothing more than for the economy and market to move away from a dependence on easy money. While central banks have made it clear they will continue pursuing easy monetary policy, perhaps the only thing to get in their way will be politics. With the U.S. election straight ahead, their job could become more complicated. While the Obama administration might benefit from the Fed’s proactive policy supporting the stock market this year, Romney has already indicated that he is not in favor of reappointing Fed Chairman Ben Bernanke.

Taken in full context, we understand and appreciate the market rise this year. As always, it is good to consider both sides of the coin. Apparently Goldman Sachs does. Goldman’s Chief Global Equity Strategist recently issued a research piece (close to the recent market high) saying that now is the best time to own stocks in a generation. At the same time their Chief US Equity Strategist has a year-end target for the market about 11% below where it currently trades. Let’s just say cognitive dissonance has become a common psychological condition for any investor these days.

The Apple Effect

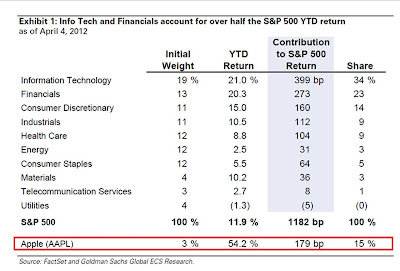

We would be remiss if we didn’t address one of the more remarkable impacts on the market: Apple.

Consider that the Dow Jones Industrial Average of 30 stocks was up about 7.5% to end the first quarter, while the S&P 500 was up nearly 12%. Also by comparison, FalkerInvestments’ equities were up about 7.5% year-to-date. Now consider that neither the DJIA nor FalkerInvestments hold Apple stock, while it is the largest component of the S&P 500. Looking at the table below, you can see that one stock, Apple, accounted for 15% of the total return of the S&P 500 Index in the first quarter! (click chart to make it bigger)

I don’t know the history, but this sounds like some kind of record. Anyway, the obvious question is: why don’t we own Apple? The simple answer is that it just doesn’t fit into our model. Clearly from an EVA perspective, it is one of the best value creators the world has ever seen in such a short period of time (their long-term history isn’t so great). However, from a valuation perspective it’s just too expensive. That may sound ridiculous with the stock up 54% in just 3 months (was it cheap 3 months ago?). But then also consider what the market underestimated then, it might be overestimating now. While not thought to be overvalued by most investors who own the stock, much of Apple’s value depends on keeping up a relatively torrid growth rate for such a large company. Who are we to doubt that Apple can continue with its recently stellar track record? (We love our i-Phones too). At the moment, Apple fits somewhere between a growth stock and value stock. Even though what they have been able to accomplish seems obvious now, it has been a speculative stock the whole time. While it’s unlikely Apple will fit our value model anytime soon, we keep a close eye on how it performs, because it just might dictate the next move in the market.

Strategy Update

Here’s an update on what we’re doing. As we said in our year-end blog post, after twelve months of zero return in the stock market, investors had generally become risk-averse and pessimistic. Entering this year we were making plans to start broadening out the portfolio, becoming more economically diversified and less defensive. As our clients are well aware, given the tumultuous and somewhat unprecedented economic events that have unfolded globally since 2008, we had chosen the path of protecting capital and focusing on dividend income. That served us well last year, providing positive returns and avoiding much of the extreme market volatility. But we have always considered that position to be temporary. Our longer-term objective is to find value opportunities across the entire market, without a bias toward any particular industry or economic sector.

We have started to execute that plan, but have adjusted our timing somewhat with the market surge. We have increased our overall market exposure (i.e. reduced our cash position) by only a few percentage points, mainly focusing on becoming more diversified. By means of explanation, consider our investments in Consumer Staples and Utilities, two of the best performing sectors in the market last year (Utilities were the best performing sector). In percentage terms, our client portfolios were roughly 20% and 14% invested in Consumer Staples and Utilities, respectively. That compares to their weights in the S&P 500 of roughly 11% and 3.5%. Much of that overweight position was afforded by our underweight positions in Financials and Industrials, two of the worst performing sectors last year, Financials being the worst. Again, with Europe’s banking system looking vulnerable to a very severe economic crisis, we avoided the chance that insolvency “over there” could impact the financial system here.

So, as one might expect with the current rally, the first quarter has seen a complete reversal of fortune for those sectors, with Utilities the worst performer and Financials one of the best (as you can see from the chart above). Therefore, our transition, while well planned, has slowed somewhat as we are, in simple terms, reluctant to “buy higher and sell lower”. However, we have made significant progress finding what we consider to be compelling values in sectors where we have been underweight. Given the strength in the market, a few of those stocks have already exceeded our expectations. While not a topic for this blog, we will relay our thoughts on new holdings during client meetings and occasional blog updates.

We will continue trimming back our exposure to the Utilities and Consumer Staples sectors as we seek value opportunities in other sectors. How much we continue to reduce our absolute cash position will be somewhat dependent on market corrections. As we gradually transition the portfolio, our goal is to own around 40 stocks that together represent all 10 economic sectors of the market. At any given time we are considering roughly 120 companies that meet our basic criteria of generating EVA while trading at relatively low valuations. Historical analysis clearly proves that a disciplined strategy of owning value-creating companies at relatively low valuations outperforms the market.

Thanks for reading. Let us know if you have any questions.

Peter and Jack

April 9, 2012